It might have been my imagination (or perhaps wishful thinking), but in the midst of this year’s back-to-school media coverage, the issue of student debt seemed a little more prominent than usual.

At least two surveys identified high levels of debt ($28K on average), and the stress — more than that of finding a job or getting good grades — this is causing students. The federal government estimates the cost of a university degree (including accommodation, tuition, food and other expenses) to be $60K for a four-year degree, while a separate survey put that figure at closer to $80K.

And every year around this time, Statistics Canada releases its revised tuition fee figures for the previous year and makes projections for the next, along with the annual percentage increase.

So, much as I appreciated the media interest in our most recent report, Eduflation and the High Cost of Learning, I have to admit I was surprised that the majority of the kerfuffle was not prompted by our Cost of Learning Index, but rather our tuition fee projections over the next four years.

After all, it’s no secret that fees are increasing. I mean, even Jeffrey Simpson is on to that one, as he made it thoroughly clear in his Globe article (alternatively titled “Duh! I so knew that already”).

Apparently he thinks that instead of documenting this trend of spiraling fees and rising student debt, we had just, you know, discovered it (note to self: add Jeffrey to our mailing list…). But I’m not going to quibble with timing; even Jeffrey Simpson accepts the fact that as public investment wanes, fees are soaring (along with the debt being incurred by students as a result).

And that was the underlying theme in so many of the interviews about the report: how is this hurting students? Not if, but how. That may not sound like a controversial shift in opinion, but believe me, it is. Because for some time, there was a convenient perception (and unfortunately, while no longer ubiquitous, it’s still out there) that a little debt was a good thing. For real. Because It Builds Character. After all, if you just “give education away for free,” the kids just won’t be able to appreciate it. Am I right?

Of course, education is not free; there are two ways to pay for it — publicly, through the tax system, or privately, through user fees. But depending on income level, one way results in significant levels of personal debt. The other allows students to “pay back” the public’s investment in their education over time, through the tax system, without being saddled with an additional private expense just as they are starting their careers and their adult lives.

There are enormous benefits to graduating a debt-free generation. After all, those with student debt are less likely to have assets or own a house; and those who do own a house are more likely to have a mortgage. Other life decisions may be postponed as well, including starting a family (or, hell, moving out of your parents’ basement). Their reduced consumer power has an impact on the economy; but so too does the spectre of a new generation that is, by necessity, singularly focused on finding a job — any job — that will allow them to begin making payments on their loan before collections agencies come calling.

The topic of income-contingent loan repayment tends to rear its head at about this point in the conversation. Why not just extend the repayment period by tying monthly payments to income? So, for example, an investment banker would pay their loan back much faster and at higher monthly payments than, say, a librarian (leaving aside the issue of compound interest, which would of course increase the total amount paid back over the repayment period. And also ignoring that income-contingent loan repayment schemes often becomes a precursor to further withdrawal of public investment and higher tuition fees being charged to students).

Newsflash: we already have an income-contingent repayment program. It’s called the personal income tax system, and it is perpetually — with built-in flexibly — tied to income. So when we download the responsibility for paying for university onto students (and make no mistake — this is a direct result of the withdrawal of public investment from 84 per cent in 1979 to 58 per cent in 2009) as well as the private debt that comes with it, we are in effect taxing them twice. Once through the tax system, and once again through debt repayment.

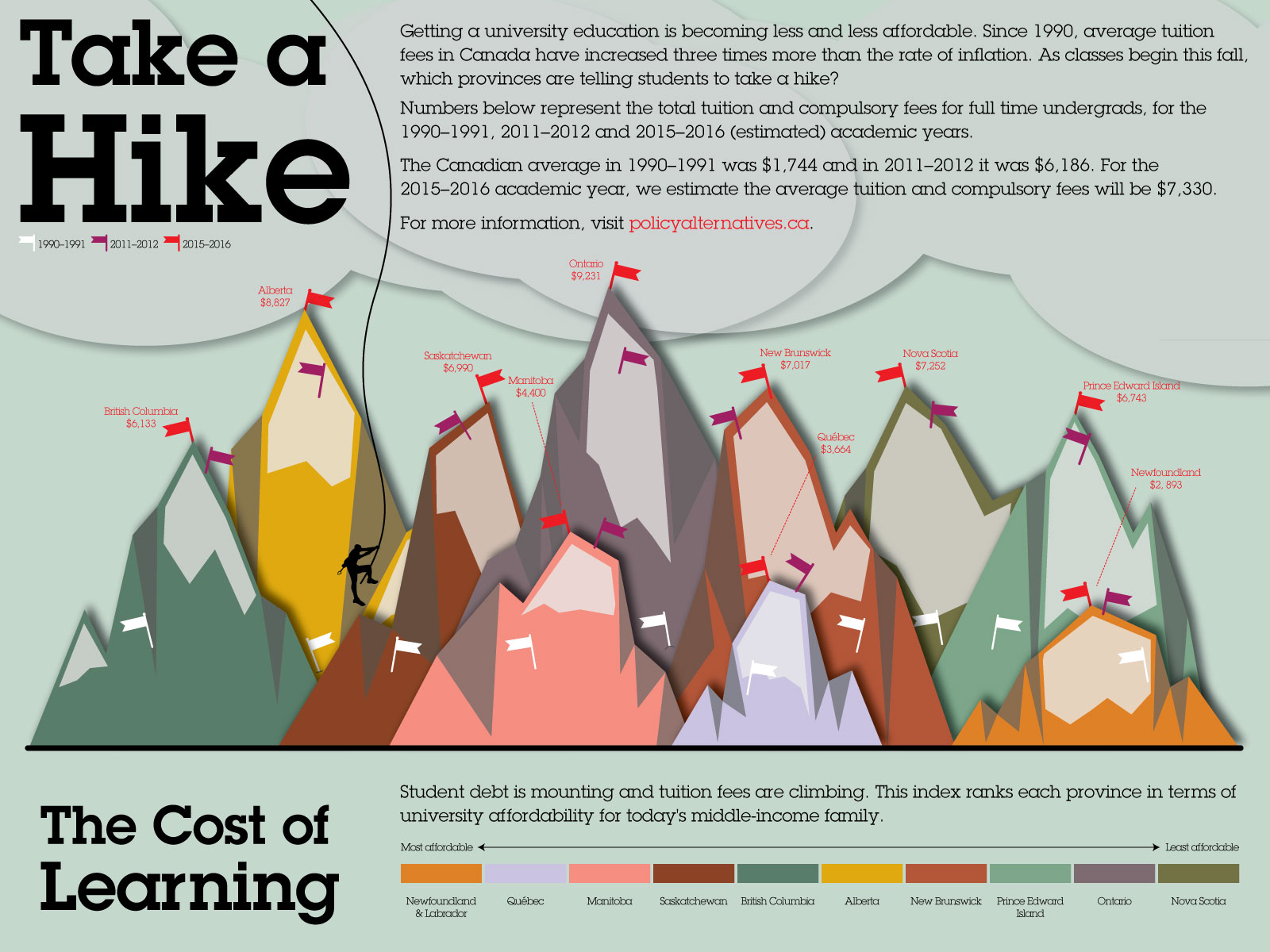

There is nothing — nothing — inevitable about this. Across the country there is an incredible range of policy decisions that have resulted in students paying less than $3,000 (Newfoundland and Labrador) or well over $7,000 (Ontari-ari-ario). And as for the “but what’s a cash-strapped provincial government to do?” refrain, Alberta’s tuition and other fees are cozying up to the $7,000 mark too.

The fact is: governments have choices to make. They can tinker with campaign-styled funding gimmicks like loans forgiveness and targeted grants and loans (“click here for your tuition rebate!”). Or they can tackle the issue of affordability directly with an upfront reduction for all students, and recognize the lasting benefits that come from a debt-free, well-educated generation eager and able to pay back the public investment in them through the tax system, and in their contributions to society.

What’s Harper up to? Award-winning journalist Karl Nerenberg keeps you in the know. Donate to support his efforts today.

Support rabble today!

We’re so glad you stopped by! Thanks for consuming rabble content this year.

rabble.ca is 100% reader and donor funded, so as an avid reader of our content, we hope you will consider gifting rabble with a donation during our summer fundraiser today.

Whether it be a one-time donation or a small monthly contribution, your support is critical to keep rabble writers producing the work you’ve come to rely on as a part of a healthy media diet.

Whether it be a one-time donation or a small monthly contribution, your support is critical to keep rabble writers producing the work you’ve come to rely on as a part of a healthy media diet.

Become a rabble rouser — donate to rabble.ca today.

Nick Seebruch, editor