You can change the conversation. Chip in to rabble’s donation drive today!

The past 18 months have seen real wages increase in Canada. (Yes, I double-checked.) Indeed, real wages have gone through two distinct phases of growth since the financial crisis hit the global economy in 2007. This may be surprising as we have been accustomed to hearing about the stagnation of real wages and the “decoupling” of wages from productivity gains over the decades preceding the crisis.

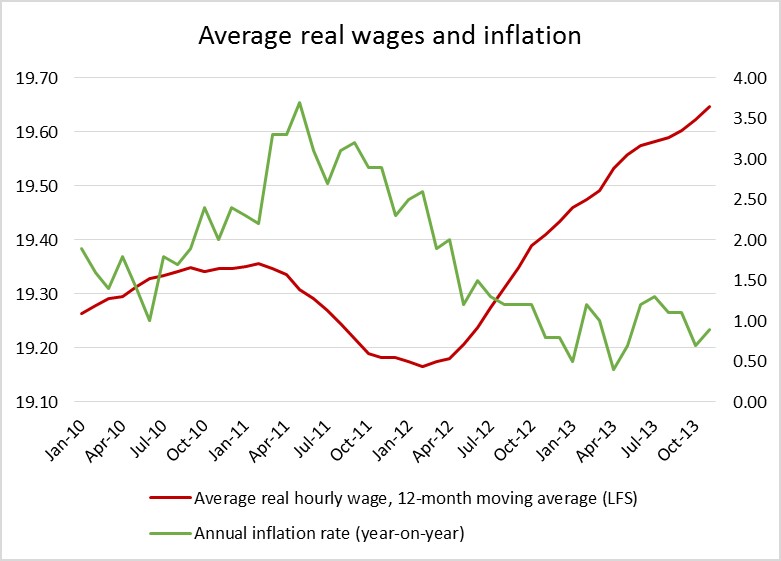

These real wage gains, however, are not that surprising once we take a look at the behaviour of inflation since the crisis. Stephen Gordon has taken a look at this over at Maclean’s; below, I offer another, somewhat different, perspective.

For much of the five-year period, inflation has been below the Bank of Canada’s two percent per year target. This despite record-low interest rates. Normally, the story goes, lower interest rates are a spur to economic activity, driving businesses to invest and expand and households to increase spending. The increased activity then generates rising prices. This story has not panned out in recent Canadian experience.

While low interest rates have led consumers to take on record levels of debt, the rebound in business investment has been somewhat tepid. For now, the corporate sector has largely taken advantage of easy money at low interest rates to issue corporate bonds and refinance loans, pay out dividends to shareholders and expand an ever-growing stockpile of cash (now totalling over $600 billion). With high profits largely unaffected by the crisis, corporations are happy to watch asset prices rise and play the waiting game to see how the “recovery” of the economy looks in the longer-term. Monetary policy and fiscal austerity measures have combined to enable this scenario.

Consumers, on the other hand, have not had the luxury of being so patient. Rising housing prices stemming from overall asset inflation and the continuing deterioration of public services are only some of the factors driving households to take on credit and spend. The current easy credit bonanza has contributed to the continuing rise in Canadian household debt, unabated since the crisis and now at over 160 per cent of income.

In a small, open economy like Canada’s, many other factors are also at play in setting macroeconomic conditions, stemming from our relationship to the rest of the global economy. For example, a slower but continuing commodity boom since the crisis that has, until very recently, maintained an elevated Canadian dollar has also contributed to keeping imports cheap and inflation down. Taken altogether, these trends have resulted in often below-target inflation and the post-crisis periods of low inflation has, as a result, coincided with periods of real wage growth.

The picture of average hourly real wages and inflation since 2010 can be neatly divided in two: one phase of higher, near 3 per cent, inflation that saw falling average real wages and a second phase of lower, around 1 per cent, inflation during which average real wages rose.

For workers it seems, the crisis has had a silver lining. As usual, however, there are several complicating factors behind this simple graph. First of all, while the unemployment rate has been slowly falling since the crisis, the last three years have also seen the employment rate drop to an even greater degree and stagnate. So even as our unemployment rate falls, our growing population and stagnant employment mean that Canadians are increasingly dropping out of the labour market completely. A not insignificant group of demoralized workers has left the labour force rather than even try to participate in the wage boom.

Second, while average real wages have risen, median real wages are actually lower than they were three years ago. In general, the median is better than the average at gauging what is happening to wages, as wage rates are unequally distributed. A wage floor compresses one tail of the wage distribution and a significant number of high-wage outliers draws out the other tail. This generally inflates the average wage. While Figure 2 shows that average and median wages surprisingly tracked each other relatively well for a while, they have now diverged again. The median worker has not seen real wages rise over the past 18 months.

Figure 2. Comparing average and median real wage growth since the crisis. Source: Statistics Canada, LFS.

This points to a greater bifurcation of the labour market with real wages growing for a smaller percentage of high-earners and stagnating or falling for a larger portion of low-earners. A recent report about Alberta’s job market describes exactly this phenomenon. The two-tier labour market in that province, where a large portion of jobs are in low-paying, low-quality service work, could rapidly become a model for the rest of the country.

Alberta also points to another factor behind the no longer quite as rosy recent wage picture: Canada’s reliance on resource exports. R&D spending by Canada’s corporate sector has dropped even further below its already low levels. R&D now amounts to just 1.7 per cent of GDP, down by almost 20 per cent from just a decade ago. Sam Gindin has pointed out that total R&D spending by Canadian manufacturers in 2012 was lower than that of General Motors on its own, which has only the 5th highest R&D budget among U.S. firms. Gindin states that the lack of R&D and a reliance on resources make Canada a “mid-tech” producer less able to quickly restructure its economy, even at the behest of significant government intervention and stimulus. Resource exports have been among the factors keeping the dollar high since the crisis, not only contributing to the loss of manufacturing capacity, but accounting for some of the real wage growth.

Yet relying on exchange rates to help boost wages is not a long-term solution; indeed, a number of factors have recently caused the dollar to change course and begin to depreciate in value. A significant fall in commodity prices over the past year — the Dow Jones-UBS Commodity Index fell 12 per cent between mid-January 2013 and 2014 — has depressed the value of the currencies of many resource exporters and surely had an effect on the Canadian dollar as well. Weak job figures and worries about continued loosening of monetary policy have also contributed to the loonie’s dive.

This, finally, brings us to the crux of the matter. Low inflation is, at best, a temporary means to raise real wages. Even when lower inflation contributes to raising real wages, as in the direct aftermath of the last financial crisis, it can be, and often is, associated with concomitant negative effects. In Canada, these have included a commodity boom that has reduced innovation and productivity growth, greater bifurcation in labour markets and monetary policy that has largely served to increase asset prices, swell corporate cash stocks and drive ever-higher consumer debt loads. As I have argued elsewhere, low inflation is one of the myths of central banking, and focusing on it to the detriment of other macroeconomic goals often means placing the interests of asset owners over workers.

Workers have simply been lucky. Higher real wages have not been the intended target of current monetary and fiscal policies that have focused on raising asset prices and maintaining profits; they have been its unintended side effect and one that the policy of monetary loosening is partly intended to reverse. Here, I agree with Stephen Gordon: our governing classes will look for any means to reduce real wages in order to ensure that any further “recovery” will help their friends in boardrooms and with stock holdings. Recovery is not their preferred term for the improved working and living conditions for the majority of working Canadians.

So, in the face of theories and practices that see rising real wages as a problem, the main driver of real wage growth can be little else than increased worker bargaining power — and this, sadly, remains as depressed as ever. Union density continues to fall in Canada and the aftermath of the crisis has not changed this. At the same time, austerity policies from federal and provincial governments have inflicted disproportionate levels of harm on working people.

The path to genuinely increasing wages runs through political renewal and solidarity. We have the tools. Standing up to austerity measures, reigniting union organizing, and imagining alternatives should be high on the list. Only when we begin to use these tools can we begin to counter absurdities such as unintentional rises in real wages. Imagine a monetary policy that rather than working to raise asset prices and grow corporate cash piles while accidentally raising real wages in the process is instead geared towards public investment in high-value-added social production that puts improving real wages and working conditions at the centre of its agenda. Now there’s an “absurdity” worth fighting for.

Like this article? Chip in to keep stories like these coming!

Support rabble today!

We’re so glad you stopped by! Thanks for consuming rabble content this year.

rabble.ca is 100% reader and donor funded, so as an avid reader of our content, we hope you will consider gifting rabble with a donation during our summer fundraiser today.

Whether it be a one-time donation or a small monthly contribution, your support is critical to keep rabble writers producing the work you’ve come to rely on as a part of a healthy media diet.

Whether it be a one-time donation or a small monthly contribution, your support is critical to keep rabble writers producing the work you’ve come to rely on as a part of a healthy media diet.

Become a rabble rouser — donate to rabble.ca today.

Nick Seebruch, editor