$$$

Issues Pages:

$$$

http://www.bnn.ca/bmo-declares-toronto-housing-bubble-amid-dangerously-h...

Toronto is a growing danger to itself and the communites surrounding it. On the page there is video that corresponds with the article, a good watch. The pundit from the bank was saying the that crazy prices gains spreading as far as peterbrough and hamilton. Personally I think the bubble is in other major communties south of toronto which surround the 401 highway as far as london.

The pundit was saying that dont worry its in toronto and the surronding communities. What I will point that the greater toronto area has population of 6.4 million as of 2016. Thats almost 1 in 5 of all canadians, thats is significant.

https://en.wikipedia.org/wiki/Greater_Toronto_Area

What about ontario? 14 million

http://www.fin.gov.on.ca/en/economy/ecupdates/factsheet.html

Thats 47% of people of ontario live in community that is experiencing a housing bubble and I think that is conservative.

I have been talking about the bubble for half a decade now. I do not know when the end will come but it with end with a ton of misery. Right toronto is growing at +20 % a year, can we reach 30% or 40% ? with a inflation rate at minus 2%. What can go wrong in this situation

Some argue that the bubble is in almost every urban area of Canada.

http://www.cbc.ca/news/canada/toronto/toronto-house-price-1.4056093

In my previous post I proposed a question just how far can market go before the crash. We I thought it would not go beyond the mid 20's. Data for the GTA month of march the average selling price was up 33.2 percent over the year. Roughly 688,000 to 916,000, I salute you brave gladitors you have truely you found a way to turn base metals into gold.

Just look at John Tory's face in the article. They all must know how this will end but there scared to be blamed for the lose of the good times. Even the big banks most be getting very worried about this but must of the money must be coming for the shadow bank sector(non traditional lenders). At this point dont worry be happy because nothing can be done mitigate the ditaster.

I think we could go maybe 45% year on year at this point.

http://www.bnn.ca/full-blown-housing-bubble-economist-alarmed-by-view-of...

There is an article and video clip association the BNN web site. I thought to myself nothing would surprise at this point in regards to the housing bubble. Here it is.

A majority of canadians 54% believe that home prices will NEVER FALL. Let that sink for a while. I watch BNN quite a bit it largely unheard to hear a guest use the word panic to decsribe the housing market in any way. And add to craziness the artilce at the bottom has a poll. 22% of those clicked the survey thought the prices would never go down. After reading the article and maybe watching the BNN clip they still think the price will not go down. My conclousion is this going end so so bady, 54% of the public will not know what hit them.

It's interesting that in 10 years as PM, Harper whose degree was in economics, did nothing about the housing market bubble. Presumably it would have endangered his power; so much for economic responsibility. The Liberals have cautiously done *something*.

This is a gem. I heard of this event in passing in the media. I reasearched this event online becasue it sounded to bubble rollcuster ride but I can not find much in the media. My search was not in vain, so I present to you the rabble viewer an example of mass delusion.

http://www.macleans.ca/economy/realestateeconomy/a-day-of-insanity-that-...

http://www.bnn.ca/home-capital-shares-plummet-osfi-monitoring-situation-...

http://www.cbc.ca/news/business/home-capital-financing-1.4086168

this home lender could be in world of hurt. Its been supplying credit to the bubble if believe that their is one.

http://www.cbc.ca/news/business/manulife-housing-debt-1.4127243

Canadian home owners are holding on with fingertips to their homes. Debt payments are getting onerous. There is a question to the methodogoly of the poll. 72% homeowners with income over 50,000 would face a percarious econoimic condition if mortages payments rose 10%. If I am doing the math correctly a current person paying 4000 in a mortage payemnts would be in trouble if they had to pay 400 more a month. When I read these stories I think Canadians are 1 recession away from an epic economic crisis. Everything is on credit and economy based on monthly payments that on based on historically low interests.

And how many years have we been hearing this now?

After all even a stopped watch tells the correct time twice a day!

And how many years have we been hearing this now?

After all even a stopped watch tells the correct time twice a day!

That is certainly good question, but I will split your question to into 2 parts. Its dependent on your economic belief.

1.Do you question the existence of capitalist business cycle(recession and boom). This is standard fare for even capitalist economists. Look up the business cycle in a google search.

a. I believe in the business cycle >>>>> Jump question 2.

b. I don't beleive in the business cycle. A recession can be kept at bay for a indefinite time. History seems to agrue agaisnt this point of view. Refer to article below.

http://www.marketwatch.com/story/current-us-economic-recovery-may-end-up...

The chart in article is very powerful exhibit for existence of the business cycle. When article was written the US was in the 84th month economic expansion. That means the US in the 94th month expanison today. 3rd longest expansion in the history of the US, in 2019 the US would break the record of 120 months expansion. Can the US set a record, I not idea. But that is not the important question, the fact is a recession is coming. Be it 6 months from now or 6 years from it will happen.

Question 2. How bad will the recession be. This debateable. My personal thoughts on the matter are buttrested by 2 factors.

a. Debt- Generally speaking during during a recession debt is destroyed. For example a business or individual go thru bankrupcty, you as indivudual or business which effectively nullify claims ago you. This of course does happen to everyone but most people buckle down and spend less and try to pay debt off. If people are losing there jobs and business are closing it makes one naturally wary of spending. The interesting thing is once you go thru belt tightening and/or bankrucpty you are ready to spend ago and partcipate in the business cycle. Claims are agaisnt are gone and you get a free start as a cog again it the capitilist cycle. From the capitalist point of view you have capacity to borrow again and spend again. Much better than weighted downed by debt which curtails spending. If things get out of hand a depression is possible. And the cycle repeats itself. Leverage up and Leverage down followed by Leverage up.

I went thru narrative that is clinical in nature, but process on human beings is one of struggle and pain.

b. Government response- Generally speaking modern governments want to stay in power so they try temper the effect of the cycle above. Monteray response means that the central back will intervene agaisnt the cycle but lowering rates and print money. To jumpstart the economy.

In the old days there fiscal reponse(Kenyism), direct spending or tax cuts into the economy by the government. This still used by the governments but oppossed by conservative thinkers. And off course buffers like EI and varoius welfare schemes saidly these ideas have been effectively demonized by the right as useless spending. But in a captialist system they used to provide 1) A buffer to the magnatude of develaging and 2) A scheme of social control to keep the status quo going, desperate people in a democracy can hinder the smooth operation of the capitalist system. Keep those nasty thoughts of class and where you begin in the economic order in check.

3. I have talked about the American economy why is this revelant for Canada. While the US effectively can resist a recession in Canada can not resist a American recession. The US economy is still largely indepentent of the effects of the world on it. Last time I checked the US imported 15 of its GDP and exported 10 of its GDP. Canada has a much more globalized economy with 33 to 36 of the tied to GDP with exports and imports. With 75 of the exports going to the US. Its getting really late, so the US buys arounds 25% of other yearly prodcution(GDP). The important thing is a US recession will drag canada into the mess.

NR Catchy talking points and boosterism aside, I refer to your comments at the beginning of the post. Can you back your ideas with some facts and ideas. You know put some meat of those bones. I tried to spell out my views in coherent way, I welcome your ideas and yours thoughts on your prespective.

http://www.crea.ca/housing-market-stats/mls-home-price-index/hpi-tool/

An excellent tool for the public want to know prices.

I was curious about wages(Average weekly earnings) in Canada and the impact of inflation. Stats Can Table 281-0063

I will discuss my methodology in the next post. Here I want to share some tidbits of wisdom.

In 2002 jan average weekly earnings were 672.10

In 2017 mar average weeking earning were 966.06

I used the Bank of Canada inflation tool. Very Cool

My conclusion was that after inflation the average weekly wage was up 10% not over 5 or 10 years. 15 years and 3 months earnings up roughly 10%, I certainly will not be doing my happy dance here.

Using HPI tool.

Average "home" was jan 2005-----$ 261,110 index 100.00

Average "home" was april 2017 ------ $ 606,000 index 232.1

Average weeking earnings in 2005 jan $ 724.67

In 2017 mar average weeking earning were $966.06

Earnings are roughly up 33%

Home prices are up 232% over that period. ERROR

It should be 132%. The index reading of 232 only represents an increase of 132%.

100% increase is 261,110 over base of 261,000

32 % increase 87,000 over base of 261,000

-------------------------------

132% =348,000 + base 261,000 = 609,000 much better.

Using the HPI Data

jan 2005 "home" price $261,000

adjust for earnings over 12 years and 4 months, the is up 33% would equal a "home" $347,130 but the "home" is actually $606,000.

How can this can this be>>>>>>> debt. Let that settle in. Any ways I felt I did not do any horrible math mistakes. This truly represents the state of affairs IMHO. Weekly earnings data was available to march 2017 while HPI was up to date to april 2017.

Two things to remember about real estate.

One, real estate prices very seldom go down, and even when they do, it's for a short period.

Two, they keep making more people, but they're not making any more real estate. Which kind of explains point One.

Tell that to Japan.

Also, it took about twenty years for prices to recover from the 1980s real estate crash in Vancouver.

Two things to remember about real estate.

One, real estate prices very seldom go down, and even when they do, it's for a short period.

Two, they keep making more people, but they're not making any more real estate. Which kind of explains point One.

I remember a dozen years ago, when my wife and I were shopping for a Toronto house, and we felt pretty lucky to find a century row house in an old, working class neighbourhood, for $300K.

At the time, I got curious and pointed the MLS listings at my old hometown of Dresden, ON, and found that I could have also bought a century farmhouse (fully detached, of course) with a bit of land around it for $66K.

Seems to me that this "bubble" is mostly about supply and demand, and necessarily has more impact in areas of scarce supply (e.g. downtown Toronto or downtown Vancouver houses) and high demand (e.g downtown Toronto or downtown Vancouver houses). This doesn't mean that most people can't afford to live in Canada, just that they might have trouble in some desireable parts of it.

Also, it's not really clear how a bank is "fuelling" this "bubble"? By continuing to issue mortgages? By following the Prime Rate?? How are they responsible for the market desire for a fully detached house in Etobicoke, but they're not responsible for our sudden fascination with fidget spinners??

From basement dweller:

Tell that to Japan.

Also, it took about twenty years for prices to recover from the 1980s real estate crash in Vancouver.

Not sure where you're getting your information about Japan from, but here's an article on Japanese real estate from this year:

Japan’s housing market remains buoyant

Japan’s housing market remains upbeat, despite slow economic growth. House prices continue to rise strongly. Property demand islargely stable, and residential construction activity is rising.

Japan’s overall residential property price index rose by 4.7% (4.2% inflation-adjusted) in January 2017 from the same period last year, according to the Ministry of Land, Infrastructure, Transport and Tourism (MLIT). Nationwide, condominium prices were up by 5.2%, detached house prices increased 2.7% and residential land prices rose by 4.8% over the same period.

Here's a graph of real estate prices in Tokyo over the last 12 years:

That doesn't look much different than anywhere else. A brief flat line around '08, but starting to climb again by five years later.

Here's a graph of home prices in Vancouver from 1977. There is a peak in 1980, and a drop back, but by 1988 prices were climbing beyond that experienced in 1980.

If you had a bought a detached home in Vancouver, even at the peak price of 1980, by 1990 you would have achieved a significant increase in the value of your home. Tell me of any other tax-free investment with that kind of return.

I was refering to the Japanese bubble for much more than 12 years ago.

Here's another historic graph of Vancouver real estate prices: <http://2.bp.blogspot.com/-ibEMy3WHmI8/UuQfWxxxFTI/AAAAAAAADfM/3fiRUSb2uH...

I think the difference is whether you adjust for inflation.

I'm also fairly sure there are parts of the United States that haven't come back to 2006 prices.

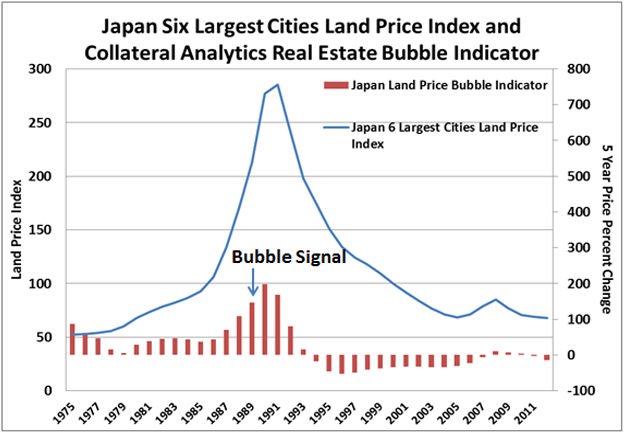

Here's a graph of the Japanese bubble. I'm not saying this is the best graph, I don't know, but this basically shows what happened:

Mr.Magoo

When I left universty I believed that money was created through the money multipier effect. Pretty standard fare even today.

https://www.youtube.com/watch?v=JG5c8nhR3LE

You will notice this addressed to "Econco Students" 2014 which means even today they still teach the following idea. Banks use reserves to create money/loan/debt and bank reserves limit the amount the money. The above provides a nice cause for banks get desposits and then loan them out using money multiper effect and money is created. What is important here order 1. Get desposts 2.Then loan them out 3. Its by default then there is barrier to fruther loan/money/debt growth based on deposits held.

This totally totally wrong banks create money regardless of reserves. I remember an article in business insider right before the crash which was taking about this and said the wrong. It claimed the banks created money/loans before getting reserves. The traditional teaching is that is opposite. At first I held on what was logicaly explaination reserves first the loans. But as researching more on the idea it lead to personal revoulationary understanding what the article was getting at. Banks can create money at while. The idea that reserves play a major role or barrier is false. When I accepted that idea. It opened me to many threads of thoughts that were closed because of false belief money multiper was true. Acceptance of this idea leads to the how banks create housing bubbles and price wars. I have stop now becsuse I am offered a free meal but I will continue when I get back.

I have stop now becsuse I am offered a free meal but I will continue when I get back.

When you come back, maybe you could take a run at my question.

Banks cannot drive the demand for houses, nor the supply of them. And given that communities as large as the GTA, and as small as towns of a few thousand have banks, why do you suppose this "bubble" exists primarily in large urban centres like Toronto and Vancouver, and not so much in Wawa or Moose Jaw?

I am getting there, but you got build a base first your agrument.

Foundation - Backs can create money at while

Next we address business model of the bank. This is simple. Banks try of maximize profits. Lending on homes is a large part of their revenue.

In the first post I explained that banks have the power make money through credit which they do a will. But there pratical lending barriers that don't something to destroy thems. So lending growth in the banks will not be for example 100% year over year clearly that would be insane. But would they make bad loans not thru malice rather hubruis, stupity, greed. Yes.

If that is all I had then even I would myself say Seeking your peddling a weak agrument. Human failings alone do not cause housing bubbles. But consider the following what if a bank was in a situation where is the most greedy and stupid loans were possible to make on the terms that if went high risk/high profit. But what if that mortage loan is guaratted to be paid if the orginal lenders fails to pay. For example you had insurance on loan and very cheap to buy the insurance on the loan. You get the full profit if the risky loan is paid but if the loan does go bad you pay a token amount and somebody else loses money on loan because bought their insurance product. Highprofit loan with very cheap insurane that is very enticing.

Sorry magoo I am falling asleep here, be pateinet you get a very well agrued argrument. But not tonight.

From Basement Dweller:

I was refering to the Japanese bubble for much more than 12 years ago.

You forgot to mention that the 'crash' from that bubble was deliberately engineered by the Japanese government. They undertook specific policies to drive down real estate prices. That is hardly a normal market.

{kind=link}