My recent column suggested that Canada implement a “Buy Canadian” strategy associated with major natural resource developments, with the goal of enhancing Canadian content in the overall value chain. Can we utilize our strong foothold in resource extraction, and try to leverage greater investment and value-added upstream in the value chain (for example, by stimulating more purchases of Canadian-made mining equipment)?

A related (and more familiar) priority would involve trying to stimulate more Canadian content downstream in the resource value chain — by stimulating more Canadian activity in the work of processing, refining, and otherwise adding value to the resources that we produce. Limiting exports of raw logs, bitumen, and fish, and requiring their processing in Canada, has been a long-standing preoccupation in Canadian industrial policy discussions.

Given the importance of mining in Canada’s current economic trajectory, it would seem to make sense for Canada to target mining equipment and other supply inputs as an industry in which a home-market effect could give the sector a head start. That home-market advantage can be experienced in various ways. The machine designers might be personally acquainted with the needs and constraints of their real-world applications. Geographical proximity can facilitate two-way interactions between the designers and users of the equipment. Lower transportation costs are another good reason why a domestic mining equipment sector should play a larger role in supplying our own mines.

Other economic research has indicated the possible benefits and positive externalities associated with a strong local machinery industry. Meric Gertler’s work has emphasized the local externalities that come from proximity between machine developers and machine users. David Robinson has documented the growth and constraints of the mining supply sector in Ontario. Daniel Poon has highlighted China’s highly interventionist initiatives in the mining and construction machinery sector as a case study in that country’s flexible and sophisticated industrial policy (see p. 8 of his working paper). Heterodox theory going back to Kaldor and Verdoorn has often emphasized the importance of innovation and productivity in the machinery sector, as a key determinant of innovation and productivity in the sectors which use that machinery (and indeed throughout the whole economy).

For all those reasons, it is a remarkable failure not only that Canada’s mining machinery industry remains underdeveloped, capable of meeting only a small portion of the mining industry’s needs in Canada (let alone globally) — but, worse yet, that Canadian governments haven’t even seriously thought about how to translate our growing resource extraction industry into a larger domestic mining machinery capability. We’ve never seriously tried to make those connections. Which explains why the vast majority of the sophisticated, expensive, high-tech equipment used in our mines is imported.

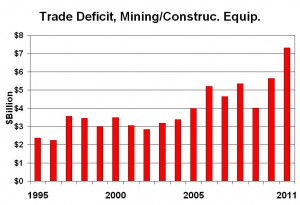

The boom in mining investment has translated into a growing trade deficit in the mining and construction equipment sector. Since 70 per cent of this type of machinery is imported, this reduces the spin-off benefits to the Canadian economy of mining and petroleum investments (since so much of the spending injection associated with those investments leaks right out of the national economy). That deficit reached over $7 billion last year, more than twice its level at the turn of the century.

Companies like Caterpillar earn billions in revenue from Canadian resource developments. Yet Caterpillar is under no compulsion to produce anything in Canada. To the contrary, our governments gave Caterpillar carte blanche to take over and then shut down important productive assets. They will continue to supply our resource projects from outside the country, unless and until we implement a strategy to enhance our capacity to do this important, valuable work ourselves.

This article was first posted on The Progressive Economics Forum.

Support rabble today!

We’re so glad you stopped by! Thanks for consuming rabble content this year.

rabble.ca is 100% reader and donor funded, so as an avid reader of our content, we hope you will consider gifting rabble with a donation during our summer fundraiser today.

Whether it be a one-time donation or a small monthly contribution, your support is critical to keep rabble writers producing the work you’ve come to rely on as a part of a healthy media diet.

Become a rabble rouser — donate to rabble.ca today.

Nick Seebruch, editor