The Bank of Canada surprised most analysts this week when it decided to cut rates by 25 basis points. The move comes after the price of oil has tumbled below $50 a barrel, oil producers announced huge cuts to business investment for 2015, Target announced a mass layoff of 17,600 workers in Canada, and the International Monetary Fund warned of a global economic slowdown.

The key message of the January monetary policy is that the Canadian economy needs stimulus. The Bank’s view of the Canadian economy stands in sharp contrast to that of the federal government, which is intent on delivering a balanced budget with a basket full of family tax cut goodies. By spending their surplus before they had even secured it, and then also sticking to an unrealistic balanced budget timeline, this government painted themselves into a corner, and made themselves look very foolish.

Thank goodness that the Bank was willing to act, and put the well-being of Canadians over concerns of a housing bubble and excess household debt.

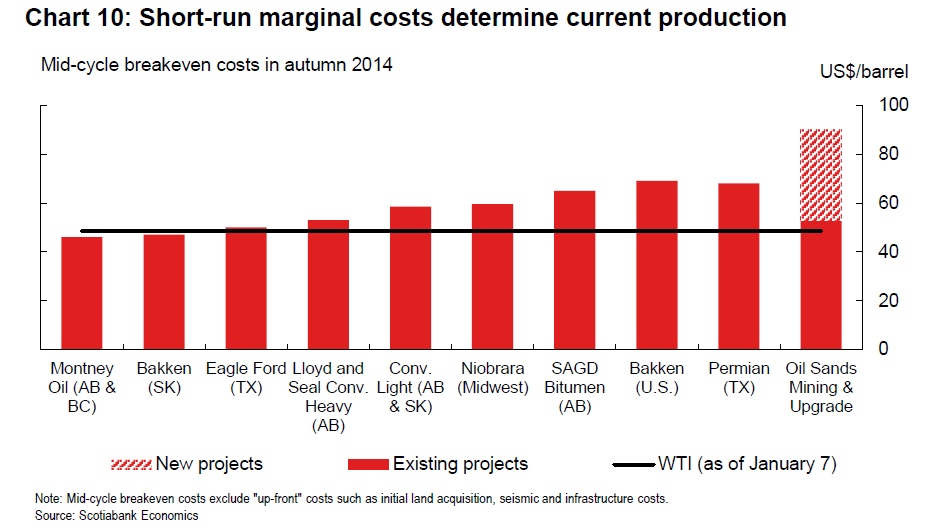

So, what was the biggest outcome of the announcement? The loonie fell to 81 cents USD, down nearly two cents on the day. It is now five cents lower than it was on January 1. Since oil and other commodities are priced in U.S. dollars, the lower loonie effectively boosts prices for Canadian commodities producers. For those that were operating at or just below their short-run cost margins, this is great news. According to the above chart taken from Timothy Lane’s remarks on January 13, that includes several sites in Canada.

While many analysts pointed to how this move was good for manufacturing, the most immediate impact of the Bank’s rate cut is to save thousands of jobs in the oil, gas, and mining sector.

As I’ve pointed out before, the benefit to manufacturing depends partly on the ability of existing manufacturing firms to grow. New entrants will be unlikely to rely on the lower dollar to stick around forever, but may be able to use the current cushion to get their projects off the ground. This will take some time. The lower dollar increases most machine and equipment input costs, so labour intensive firms actually have the advantage in the current environment.

The Bank issues its next rate announcement in March, and many observers are considering the possibility of another rate cut at that time. What is that likely to depend on? Well, the Bank based their estimate on $60 oil, and it’s currently below $50. The price is unlikely to rise until something gives on the supply side. Canadian and American producers are currently saying that their production will increase this year, just at a slower rate than last year. Saudi Arabia seems intent on keeping supply high until it forces some of those North American producers out of the market. If the price of oil stays low for the next couple of months, we could easily be looking at yet another cut from the Bank. Would it be enough for Stephen Harper to give up on a balanced budget? That’s a tougher question.

Support rabble today!

We’re so glad you stopped by! Thanks for consuming rabble content this year.

rabble.ca is 100% reader and donor funded, so as an avid reader of our content, we hope you will consider gifting rabble with a donation during our summer fundraiser today.

Whether it be a one-time donation or a small monthly contribution, your support is critical to keep rabble writers producing the work you’ve come to rely on as a part of a healthy media diet.

Become a rabble rouser — donate to rabble.ca today.

Nick Seebruch, editor