Like this article? rabble is reader-supported journalism. Chip in to keep stories like these coming.

![]()

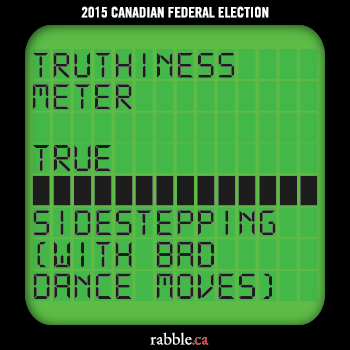

Claim: Opposition leaders pointed to second-quarter statistics released today which confirmed Canada is in a “technical” recession. Meanwhile, Joe Oliver referred to the economy’s “buoyant” June. What should the average Canadian take from this?

Canada is in a recession albeit a teeny, tiny one. The numbers released by Statistics Canada today confirm that the economy is shrinking.

The recession, like the deficit, is a political object that the parties use to advance their vision of Canada. Stephen Harper wants to run this election based on his economic record. Because of this, today’s numbers do matter: if Harper takes credit for good economic times, surely he’s on the hook for bad economic times too.

But Canada’s GDP shouldn’t be the most important marker of how Canada is doing, economically, because there are better ways to determine whether or not people are struggling in their daily lives. How politicians address these issues is much more important than squabbling over how big or how teeny tiny our recession is.

For example, retail spending in May and June was up in 2015, as compared to 2014 (especially in the used car market), though has been in moderate decline over 10 years. To finance this spending, Canadians are dipping deeper into debt. Household debt (including mortgages) is 163.3 per cent of income (it was in 1997 that Canadians passed the 100 per cent mark).

Canadians pay a lot of money in interest. On average, a mortgage will cost $60,000 (highest in British Columbia at $96,000). And, average debt reached $26,768 in 2013. While paying money to borrow money can really hurt families, it’s definitely helped one industry in particular.

In 2013, the Canadian banks “delivered” record combined profits of $29 billion. Nearing the end of 2014, they made record profits again, but warned that the good times might not last. Scotia bank laid off 1,500 workers just to be sure. And, in case you started to feel bad for the banks, mid-year reports from 2015 have showed that (don’t worry) the banks will have another record-breaking year of profits.

Canadians are helping to buoy these profits through a buffet of new or higher user fees.

The most immediate way to feel the economy for most people is through their work. Unemployment statistics can tell part of the story (though they exclude data about unemployment on reserve), but they often can’t comment on the quality of work available. With precarious work becoming more normal and tactics from employers to keep employees working in shifts that won’t let them work enough hours to make enough money to live and that reduce their quality of life.

Which party will be best for working people? Which party will stand up to the banks and regulate their user fees? Who has the best plans to improve the employment market?

These are more important questions than most of what is related to this morning’s recession numbers.

Verdict:

Photo: flickr/ frankieleon

Support rabble today!

We’re so glad you stopped by! Thanks for consuming rabble content this year.

rabble.ca is 100% reader and donor funded, so as an avid reader of our content, we hope you will consider gifting rabble with a donation during our summer fundraiser today.

Whether it be a one-time donation or a small monthly contribution, your support is critical to keep rabble writers producing the work you’ve come to rely on as a part of a healthy media diet.

Become a rabble rouser — donate to rabble.ca today.

Nick Seebruch, editor