Last month’s over-the-top “celebrations” of the 25th anniversary of Brian Mulroney and Ronald Reagan’s signing of the Canada-U.S. Free Trade Agreement seemed strained, to my mind. The self-congratulation and back patting struck me as rather overdone, contrived even. Remember, this wasn’t the 25th anniversary of the FTA’s implementation (that won’t occur until Jan. 1 2014). It was only the anniversary of its signing — by two defining neoliberal figures in 1987, a year before the famous free-trade election of 1988 decided the outcome. So in that regard, it’s not surprising that the rhetoric around the anniversary was more political than economic. FTA boosters spoke of Canada’s “coming of age,” our “new national confidence,” and other equally metaphysical effects. And the Harper government (led by International Trade Minister Ed Fast) cited an assumed consensus regarding the benefits to Canada of free trade to reinforce the irrationality of those few “free trade deniers” who still refuse to jump on board the free trade bandwagon.

In fact, I think the whole orchestrated hoopla was carefully designed as part of the Harper government’s strategy to brand Thomas Mulcair and the NDP as economically illiterate and dangerous, and hence unworthy of being a government-in-waiting. Mulcair’s understandable efforts to avoid being painted into that corner explain the NDP’s evolving positioning on trade policy issues (an evolution which I view with some caution). The boastful, if refreshingly honest, claim by Thomas d’Aquino that it was him and his CEO friends who made the whole thing happen (via what he called “bold executive leadership,” and what others might call backroom corporate dictatorship) reinforced the atmosphere of ideological manipulation surrounding the whole phony occasion.

But why don’t we take a hard look at the central assumption behind the chest-thumping of FTA advocates? Is it really so obvious, beyond argument, that the FTA has been clearly beneficial to Canada? Endlessly and loudly repeating this claim, and ridiculing and belittling those who don’t accept it, does not in itself make it true.

Here is my recent column which raised questions about the absence of verifiable macro-level benefits from the Canada-U.S. FTA. Below I provide additional empirical evidence regarding the summary statements made in that column.

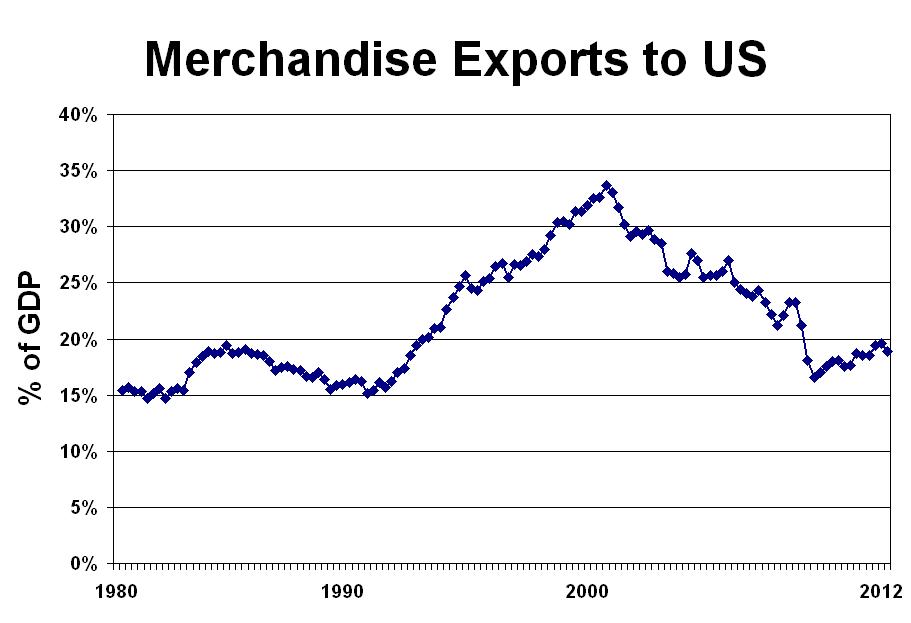

U.S.-bound exports grew dramatically in the initial years after the FTA was implemented. As shown in Figure 1, during the 1990s, they more than doubled as a share of Canadian GDP (peaking at 35 per cent in 2000, when Canada’s auto industry and other export-oriented manufacturers were firing on all cylinders). We can debate how much of that initial increase was due to the FTA (surely much of it was), and how much was due to other factors (including the low dollar, also clearly important). But it’s moot, because the trend reversed itself dramatically after the turn of the century. 9-11 sparked a U.S. recession and thickened the border. Global commodity prices took off beginning in 2002, sparking a reorientation of Canadian economic development around resources. That also lit the fuse for a 60 per cent appreciation of the currency, which has further hammered Canadian trade performance. The 2008-09 financial crisis and recession deeply shocked our U.S.-bound exports.

Lo and behold, we are right back where we started. U.S.-bound merchandise exports now equal under 20 per cent of Canadian GDP. (Those “export shares,” as Erin Weir will quickly point out, are misleading because they contrast a gross value, exports, to a net one, GDP — but they’re the most common measure of trade reliance.) That’s exactly where they were when the FTA was negotiated in the mid-1980s. Canada has experienced an astounding “deglobalization” (by this measure, anyway) that has many causes. The FTA hasn’t stopped this from happening. And to the extent that the FTA laid the institutional foundation for the resource export boom (which in turn contributed so much to Canada’s deindustrialization and deglobalization), then the FTA is indeed part of the problem behind Canada’s flagging exports.

The previous data considers merchandise exports only. Services trade is often heralded as the wave of the post-industrial future. This is nonsense, of course. Most services are not tradeable (despite call centres and other breakthroughs). More importantly, services exports have followed broadly the same trend as merchandise exports, anyway — and for similar reasons. Figure 2 indicates that Canada’s services exports to the U.S. grew gradually during the 1990s (as a share of GDP), but have declined ever since. They were still slightly higher (in 2010, most recent data available) than in 1990 (earliest data available), but only by about one-half of a per cent of GDP. And Canada has endured a large and growing deficit in its bilateral services trade with the U.S. throughout the period (that reached $14 billion in recent years).

Figure 2. Source: From CANSIM Tables 376-0036 and 380-0016.

The composition of Canada’s exports to the U.S. has deteriorated in structural terms during the FTA period (and especially since the turn of the century). This also reflects the effects of the resource boom and associated deindustrialization. Figure 3 indicates U.S.-bound exports within eight primary product classifications (at the two-digit level) as a share of all U.S.-bound exports. The eight product codes included are standardized chapters 1-5 and 8-10, and include live animals, vegetables, fats, food, mineral products, raw hides, wood, and pulp and paper. The share of just these eight groupings has increased by half since the turn of the century; they now account for 45 per cent of all U.S.-bound exports. If we include other barely processed resource-based products (such as bulk non-ferrous metals), then well over one-half of Canada’s U.S.-bound exports now consist of unprocessed or barely processed resources.

Despite this deterioration, the qualitative composition of Canada’s trade with the U.S. is still much better than it is with the rest of the world. With other trading partners (such as Europe and Asia), our bilateral trade conforms very closely to our stereotype as an exporter of raw resources, and an importer of sophisticated value-added products. Canada’s U.S.-bound exports of automotive products (virtually all of which go to the U.S.) and other value-added products have historically provided a bit more structural balance in our bilateral relationship with the Americans. But remember, our stronger export performance in value-added products with the U.S. existed long before the FTA, and was the result of either geographic proximity or else pre-FTA policy interventions (such as the Auto Pact) that have been undone by 25 years of hands-off policy. The structural composition of our exports to the U.S. has therefore substantially deteriorated under the FTA. Not only are we exporting no more to the U.S. than we were before the FTA, we are more reliant on unprocessed resources.

Figure 3. Source: From Industry Canada Strategis database, Trade by Product. Earliest data 1990.

Like Figure 1, Canada’s reliance on the crucial U.S. market as the dominant destination for our exports also rose and fell during the free trade era. At the time of the FTA’s implementation, the U.S. accounted for around three-quarters of all Canadian exports (Figure 4). That share rose to 85 per cent in the initial years after the FTA (as Canadian plants — those that didn’t close, anyway — reoriented their production toward the continental marketplace). But Canada’s deindustrialization since 2002, and the erosion of our higher-value-added exports (almost all of which went to the U.S.) has brought the reliance on the U.S. market back down to the same level it was before the deal. Here, too, it is hard to see what if any permanent impact the FTA has had. In general, the more diversified our export markets, the better: we don’t want to be too dependent on what happens in the U.S. for our own economic fortunes. But in this case, the reduction in our dependence on the U.S. market since 2002 is a symptom of an underlying weakness (namely, the dramatic erosion of our value-added exports in general), not something to celebrate.

Figure 4. Source: From CANSIM Tables 380-0063 and 228-0002.

Another ratio of interest is Canada’s share of the overall U.S. import market. The argument for the FTA was that it would give us privileged, protected access to that lucrative market. Since the turn of the century, of course, that market has not been nearly as “lucrative” as it once was believed. But more fundamentally, Canada’s share of U.S. imports has actually declined significantly under the FTA, not grown. Our share of U.S. imports did increase modestly in the initial decade after the FTA was implemented (by 1-2 percentage points), as illustrated in Figure 5. More recently, however, that market share has been cut by almost a third: to barely 14 per cent of all U.S. imports today, from almost 20 per cent in 1996. Our share of all U.S. imports is now 4 points lower than it was when the FTA was implemented. This decline reflects both the decline in Canadian exports to the U.S., as well as the surge in U.S. imports from other suppliers (notably, of course, China).

Figure 5. Source: From U.S. Census Bureau; Exports, Imports and Trade Balance by Country.

Productivity in the Canadian business sector has always been lower than in the U.S. Canada steadily and substantially closed the gap during the postwar golden age, rising from 70 per cent of U.S. levels to over 90 per cent by the mid-1980s (see Figure 6). That’s exactly when the Macdonald Commission recommended a comprehensive FTA with the U.S. — motivated largely by the assumption that it would foster the elimination of that residual productivity gap. And the economic models trotted out to support the FTA during the subsequent historic debate almost uniformly assumed that the productivity gap would indeed disappear — generating a significant productivity boost for Canada (and hence income boost for Canadians). Fat chance on both counts.

Almost as soon as the FTA was being negotiated (let alone implemented), Canadian relative productivity began slipping. The resource export boom of the 2000s accelerated that trend dramatically for a number of reasons. First, non-renewable resource extraction demonstrates secularly declining productivity, for concrete Ricardean reasons (as easier deposits are exhausted, subsequent reserves require more effort to extract). Second, the resource-driven appreciation of the exchange rate has sparked a massive reallocation from tradeable to non-tradeable sectors (as evidenced in the data above), where productivity is much lower: fast food restaurants, retail, and other small businesses. Finally, the willy-nilly management practices associated with the gold-rush-style development that has typified northern Alberta and other resource-dependent regions is hardly good for productivity.

Today, incredibly, Canadian productivity in the business sector is just 70 per cent of U.S. levels. That’s a low as it was as the end of World War II, when Canada was a poor backwater compared to the U.S.

Figure 6. Source: Centre for Study of Living Standards, Aggregate Income and Productivity Trends: Canada vs United States, Table 7a.

With stagnating productivity, it is no surprise that real incomes have also stagnated. The notable decline in labour’s share of GDP since the late 1970s hasn’t helped on this score: not only is GDP per worker growing very slowly, but the worker’s share of what they produce has declined. Real wages are no higher than in the 1970s, and neither are family incomes. Figure 7 plots real median family income (for all family units, in 2010 dollars): the 2010 figure was exactly the same as the 1980 level. Three wasted decades, as far as family incomes are concerned.

One Twitter commentator complained that using family income (rather than per capita income) might skew this analysis, given the modest decline in average family size that has also occurred over this period. But real hourly wages (not dependent on family size) have fared no better. What income growth has occurred in Canada (that has been barely sufficient to pull up average per capita incomes at all) has been concentrated in non-labour income, and among very high-income households. I think it’s reasonable to assert that the typical Canadian is no better off (in real incomes) than they were when the FTA was implemented. This conclusion of overall income stagnation over the last quarter-century is robust across various measures, and has been reported in many studies.

Figure 7. Source: CANSIM Table 202-0411.

In sum, the promise that free trade would induce more trade, productivity growth, and higher incomes (following traditional Heckscher-Ohlin mechanisms) is not remotely supported by the aggregate economic data. FTA defenders will critique this argument on many grounds. They say we should compare this data to an unknowable counterfactual (namely, where Canada would be in 2012 without the FTA), rather than to the pre-FTA reality. They will parse detailed sub-sector data to find evidence that productivity grew relatively faster in those industries which experienced larger tariff reduction, compared to other sectors. (Daniel Trefler has done much work in this vein — but it doesn’t negate the fact that overall Canadian productivity has languished.) These arguments do not alter the finding that the FTA has not been associated with more trade, higher productivity, or higher incomes — contrary to the promises made when it was implemented. And hence the promises now being made that more FTAs (with Europe, Korea, India, or the entire Trans-Pacific region) will do just that, must be viewed with disbelief.

So it is not the “free trade deniers” (like myself) that inhabit a fantasy world. No matter how loudly Trade Minister Fast asserts that only an economic illiterate would dare to question the virtues of free trade, it’s his side of the debate that relies on faith, rather than fact.

Jim Stanford is an economist with CAW.

Support rabble today!

We’re so glad you stopped by! Thanks for consuming rabble content this year.

rabble.ca is 100% reader and donor funded, so as an avid reader of our content, we hope you will consider gifting rabble with a donation during our summer fundraiser today.

Whether it be a one-time donation or a small monthly contribution, your support is critical to keep rabble writers producing the work you’ve come to rely on as a part of a healthy media diet.

Become a rabble rouser — donate to rabble.ca today.

Nick Seebruch, editor