Kudos to Bank of Canada Governor Mark Carney for raising the profile of the over $500 billion Canadian corporations are holding in excess cash surpluses and not investing in the economy, which garnered front-page coverage (and kudos to the CAW for inviting him to speak.)

It’s not the first time he’s raised this concern. Last year at the Empire Club he told assembled business leaders that their companies were in “rude health, have the means to act — and the incentives,” urging them to invest their surpluses. After cutting corporate tax rates, Finance Ministers Flaherty and Duncan have also demonstrated frustration with Canadian businesses for not investing enough in the economy and urged them to invest more.

Contributors to this blog, including Jim Stanford, Erin Weir, Andrew Jackson and myself have raised concern about corporate Canada’s growing corporate cash hoards and surpluses for much longer.

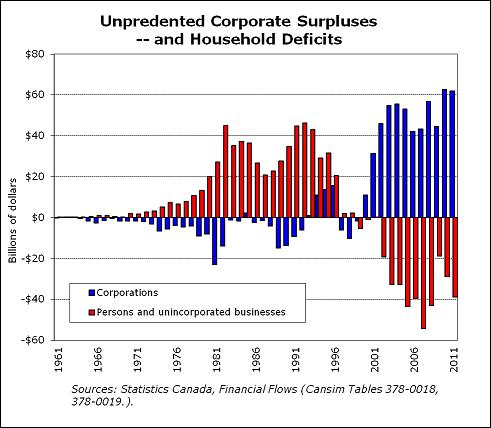

It’s important to recognize that this half a trillion didn’t just fall from the sky into the corporate coffers. As I pointed out on page 6 of this piece published in early 2007, the growing corporate surpluses ($300 billion at that time) represented an unprecedented shift in the balance between household and corporate sectors.

Prior to a dozen years ago, Canada’s household sector had traditionally run surpluses which were then lent to corporations to invest in the economy. As a result of slow wage growth, high profits, corporate tax cuts, rising house prices, and slow rates of business capital investment, that relationship completed changed around 2000 — and it’s got much worse. Above is an updated version of the slide, which I’ve used in many presentations since.

The flip side of the growth of these unprecedented corporate surpluses and the resulting growing cash hoards is of course record rates of household indebtedness — which is a major threat to our economy. While there’s always alarmism about government sector deficits, one of the underlying problems that helped cause the crisis and is a factor in our slow rates of growth was this imbalance and the growing rates of household indebtedness.

It’s not just Canada, but similar trends occurred in the U.S. and Europe. And it’s a double-edged sword. While CEOs may claim their surpluses and cash hoards are a buffer against economic uncertainty (as Matt Campbell did in the Globe), much of the non-financial corporations surpluses ultimately went into the increased financial speculation that caused the financial and economic crisis. In these ways, it’s not “dead money” any more than zombies are dead: it’s money that, while seeming to keep their hosts alive, has played havoc with the rest of us. Even the OECD and the IMF now seem to recognize to some degree that growing inequality of income (and between sectors of the economy, which is related) is bad for the economy.

Our finance ministers have used tax cuts, low interest rates, wage suppression, deregulation, etc. etc. ostensibly to get corporations to invest more of their profits and surpluses in the economy — but it hasn’t worked. Now they (and Carney) are trying to use moral persuasion, but that’s unlikely to work either.

Capitalism, in its different forms, isn’t supposed to be swayed by any morals beyond its own: maximizing short-term profits. If CEOs don’t see any potential reward for making an investment (whether through profits or personal reward through share buybacks and stock options), then they aren’t likely to do it. And if there’s a lack of demand for their products, then they aren’t going to invest.

Returning excess cash to shareholders, as Carney urged them to do if they aren’t going to invest, isn’t going to help much either. While pension funds could also benefit, much of this will go to the wealthiest in society. This will not only lead to less economic stimulus (as they have a lower propensity to spend), but it will also increase inequality and economic instability — as even the IMF, OECD and Conference Board now recognize. And if the wealthy are to invest it, where would they invest it: back into companies that aren’t investing in the economy, speculative financial investments, or into more real estate, blowing up that bubble even more?

There’s a simple and straightforward solution. If corporations aren’t going to invest despite all that’s been provided to them, then governments should tax these surpluses back through various means and use the revenue to increase public investment in the economy and redistribute the wealth to reduce inequality including by expanding public services, which will go a long way to improving the precarious state of household finances.

(Of course, we’re not going to get much of this from most of our existing governments. With the failure of supply-side economic policies in stimulating investment and the economy, I expect that Flaherty and Co. will instead accelerate privatization and P3s in their coming budgets: essentially handing over public assets and investment opportunities at the public’s expense on a platter to private business who are failing to invest money into the private sector.)

This article was first posted on the Progressive Economics Forum.

Support rabble today!

We’re so glad you stopped by! Thanks for consuming rabble content this year.

rabble.ca is 100% reader and donor funded, so as an avid reader of our content, we hope you will consider gifting rabble with a donation during our summer fundraiser today.

Whether it be a one-time donation or a small monthly contribution, your support is critical to keep rabble writers producing the work you’ve come to rely on as a part of a healthy media diet.

Become a rabble rouser — donate to rabble.ca today.

Nick Seebruch, editor