On April 16, Finance Minister Chrystia Freeland will present a Federal Budget that is supposed to simultaneously present the government’s pitch to the public for re-election and demonstrate fiscal restraint. How are they to accomplish both?

Neoliberal pundits were quick to proffer their answer: solve low productivity by becoming more enticing to big capital. We’ve been too hard on capitalists, they told us, who are our only hope. Goldy Hyder of the Business Council of Canada moaned “when did profits become a bad word in a democracy that celebrates free enterprise and celebrates capital?” And then, quite truthfully: “You know what? Capital just moves.” Past Conservative and Liberal cabinet members Lisa Raitt and Anne McClellan of the so-called Coalition for a Better Future beat a similar drum. McClellan, at the top of her lungs, pushed “talking about the private sector, and helping Canadians understand that making a profit and being successful and being a Canadian champion is a good thing.” We can’t generate more productivity until we assured capitalists we loved and needed them, viewing their profits as our collective rewards.

It was astonishing propaganda in a year in which corporate gouging accounted for a lion’s share of the inflation crisis, private equity crushed staple brands like Tim Hortons, while already extreme wealth inequality expanded. Additionally over 20 per cent of GDP is now in real estate, coinciding with the massive expansion of the financial sector; profitable private sector activity to be sure, but enormously comprised of economic rent collection that leeches investment from the productive economy. Even the remaining productive investors, meanwhile, are often, as Hyder revealingly articulated, footless absentee owners, and happy to leave a community in the blink of an eye if a better deal—or bribe—is offered elsewhere.

We should believe him.

Even if these weren’t wealthy lobbyists in the guise of concerned working citizens, there isn’t much appeal in these pundits’ promotion of trading in one paternalism over another, in this case supposedly trading government paternalism for corporate paternalism. Worse still, it does nothing whatsoever to address the looming catastrophe facing Canadian industry: the Silver Tsunami.

Over the next decade, $2 trillion of Canadian assets are set to change hands due to the retirement of baby-boomer entrepreneurs. That accounts for some 76 per cent of small Canadian enterprises, the community pillars that are not controlled by footloose absentee investors. At the present moment, only nine per cent of these owners have succession plans in place. As Dr. Sean Geobey told me on the Community Wealth Canada Podcast, buyers for such companies are extremely hard to find since small businesses are usually only attractive to those in the same field. While big companies are often owned by non-working investors who can simply hire a CEO, small businesses typically make sense for involved owners with a specialized knowledge of their industry.

The result, already underway, is that these companies are simply closing down, with jobs, community hubs, and, as the process accelerates, entire economic ecosystems of producers and purchasers thrown away.

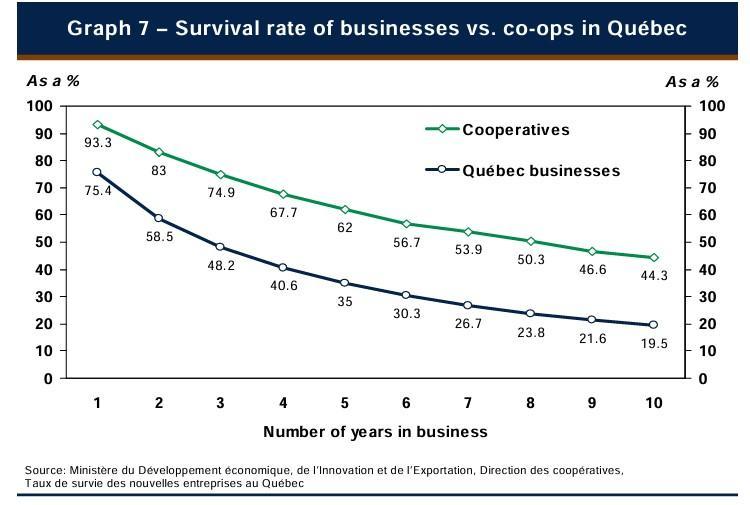

There is, however, a potential solution that can help address a great many of our problems at once. Allow me to propose, in these polarized and partisan times, a practice that could be characterized as much as “progressive conservatism” as anything else. Under our paternalistic punditry lies a remarkable economic secret: worker-owned companies, worker cooperatives, and other consumer/producer cooperatives are more successful as enterprises than standard business. In fact, research in Quebec has found that cooperatives—an ideal model for small and mid-sized business—are more than twice as likely to survive 10 years or more than standard business.

(This includes various kinds of cooperatives, but Quebec’s worker-cooperative development has patterns of success in keeping with the broader trend.)

Let the implication sink in for a moment. This is before we go into equality, fairness, democracy, good for the social fabric, and all the invaluable humanistic reasons we typically talk about such enterprises. At the crude harsh level of “is this company likely to be successful enough to survive?” inclusively-owned companies beat the mean—despite being disproportionately started by the underprivileged. In fact, worker-owned companies are routinely and globally associated with more productivity, profitability, and resilience in recessions, as well as higher wages and job retention. This is probably for fairly simple reasons, like the ones John Stuart Mill pointed out nearly two centuries ago: when workers are owners of the company, the principle-agent problem of conflicting self-interests diminishes and the entire workforce is more motivated to make the company succeed.

Worker-ownership is also remarkably popular across the spectrum. A 2019 University of Chicago survey asked 1,500 Americans of diverse backgrounds if they would rather work for a) a state-owned company; b) a company owned by outside investors (a la Hyder, Raitt & McClellan); or c) companies owned by their workers. An astonishing 72 per cent said they would rather work for an employee-owned company, including 74 per cent of Democrats, 72 per cent of Republicans, and 67 per cent of independents.

So much for polarization.

A 2021 Harvard Business Review paper, meanwhile, found that the results of halfway-normalized employee ownership could completely transform an economy. Looking at what would happen if just 30per cent of American companies were at least 30 per cent employee-owned—a seemingly minor reform—they calculated that the wealth of the bottom half the population would quadruple, Black American wealth would increase eight-fold, Latino-American wealth twelve-fold, there would be gains for the bottom 90 per cent of the population, with only the top one per cent seeing (minor) losses.

Employee-ownership and worker-cooperative are similarly distinguished in their success in company transitions. In Italy, where only 48 per cent of start-up enterprises last three years or more, the Marcora Law helps workers buy out their companies if they are set to close. In stark contrast to standard business some 87 per cent of such companies—which would have been lost otherwise—survive at least three years from the time of the buyout. This trend is not just among small businesses either: Bob’s Red Mill, one of the biggest whole grain producers in the world, transitioned to 100 per cent employee-ownership between 2010-2020, and is now completely owned by some 700+ workers.

I wasn’t kidding when I called this progressive conservatism. This is the progressive and effective way to conserve the homegrown, locally-owned market sector. Cleveland’s Fund for Employee Ownership, born out of the remarkable Evergreen Cooperatives, has been doing exactly this in recent years, saving community staples by providing capital for employee buyouts. Right before our noses is a group of people with a vested interest in their company’s continued success, with the requisite expert knowledge of its industry, who won’t, like absentee corporate investors, be looking for excuses to get up and leave. The thing they are missing…is capital.

We should empower workers to invest in themselves.

Urban economist Jane Jacobs famously argued that ascending economies came from having many interrelating small parts, like an ecosystem, and not dependence on a few big industries. In her classic 1969 work The Economy of Cities, Jacobs mused on what would happen if $300 million of government spending—a seemingly miniscule amount compared to the costs of fighting poverty from lack of enterprise—had been offered as loans for new businesses in struggling communities. She calculated some 10,600 loans ranging from $10,000 to $1,000,000 could have been provided.

As the Canadian government unveils the details of its half a trillion-dollar budget, the same concept could be applied to helping workers fund themselves. A mere $1 billion in direct grants to help workers start new worker cooperatives, expand existing worker-owned companies, and purchase existing businesses with retiring entrepreneurs could foster billions more in secure loans and fundraising.

Better still, the billion could come from a windfall tax on the piles of economic rent collected by covid profiteers. Redistributing this rent to workers as cooperative capital, empowering them to “buy in” to their own economies rather than selling out their economy, could be just the trick to reverse the trend of growing wealth inequality.

Investing in employee-ownership could help address the silver tsunami, start more enterprises, conserve existing businesses, reduce inequality, and buttress democracy. Breaking the stranglehold of paternalistic economics, meanwhile, might even help heal our social wounds.

So why not help workers help themselves?

Support rabble today!

We’re so glad you stopped by! Thanks for consuming rabble content this year.

rabble.ca is 100% reader and donor funded, so as an avid reader of our content, we hope you will consider gifting rabble with a donation during our summer fundraiser today.

Whether it be a one-time donation or a small monthly contribution, your support is critical to keep rabble writers producing the work you’ve come to rely on as a part of a healthy media diet.

Become a rabble rouser — donate to rabble.ca today.

Nick Seebruch, editor